Opontia: Aggregating E-Commerce in Unique Markets

Solopreneurs are all the rage these days, and one of the most interesting instances is that of the e-commerce entrepreneur.

Across the world, individuals are creating and selling products online at rates never seen. The Covid-19 pandemic was, in particular, a catalyst for the activity. Three separate megatrends converged:

E-commerce platforms like Amazon and Shopify proliferated around the world: these players could help single-person shops warehouse and distribute products in a way that was not quite possible until just now.

Consumers found themselves increasingly needing to purchase online: as people found themselves increasingly at home during the pandemic and forced to shop online, niche products became more attractive than ever.

Sellers increasingly found themselves needing extra sources of revenue: producers who traditionally would sell their products in-person had no other way to recover their lost revenue than to go online.

The numbers speak for themselves. Amazon’s marketplace grew to a massive $300 billion GMV in the last 12 months. And it’s not just Amazon. Around the world, e-commerce marketplaces have grown in a massive way recently.

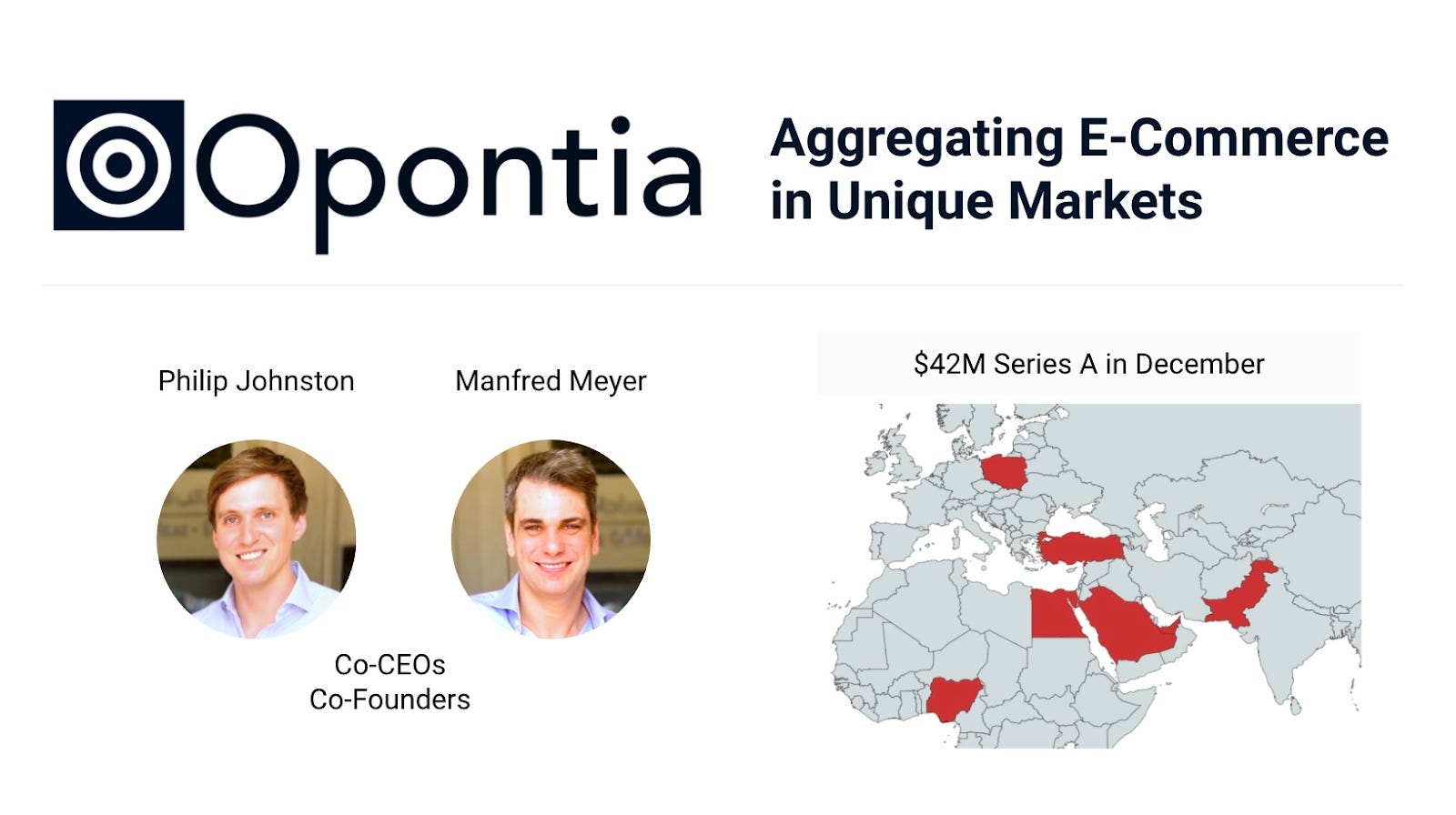

Enter Opontia. Founded a little under a year ago in early 2021, the e-commerce aggregator based in Dubai is taking off.

First, in July it was reported that it raised a seed round of several million dollars. Then, in December, the company has raised a fresh $42M. How did the company gain so much ground, so quickly?

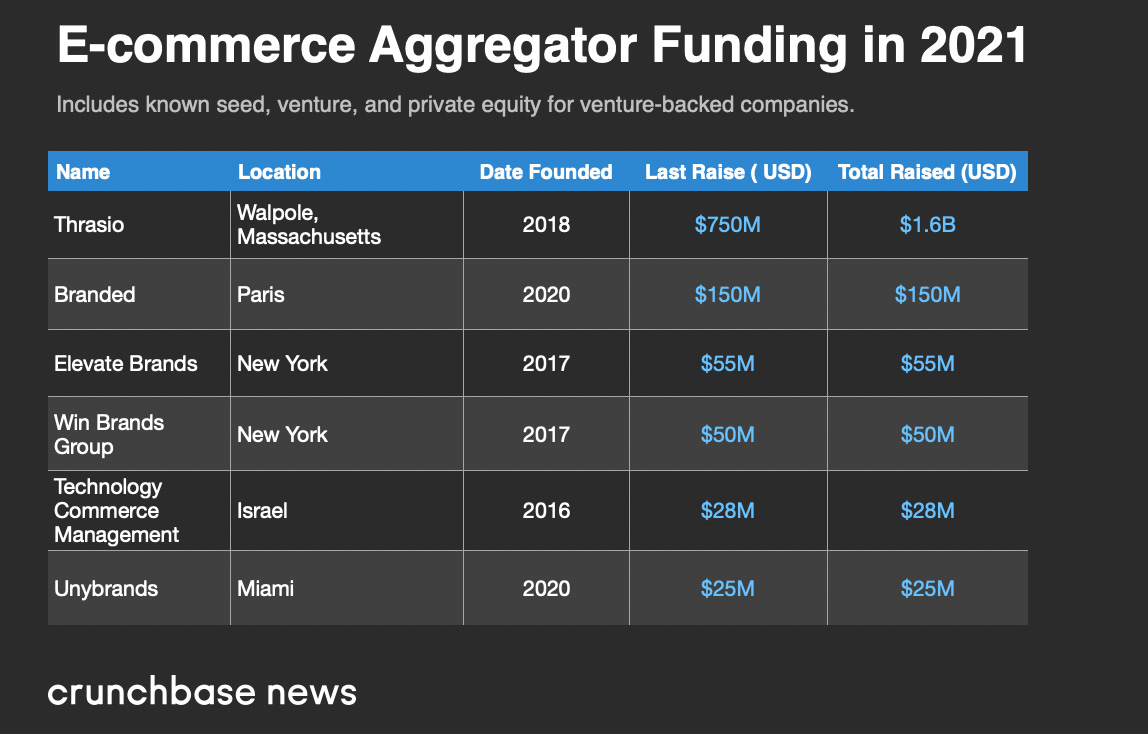

Well, for one, Opontia is not the only e-commerce aggregator gaining ground fast. It’s a fast-growing market. Companies from Thrasio in the US, Merama in Latin America, to Berlin Brands Group in Europe are also scaling rapidly. Thrasio raised over a billion dollars last year. Merama achieved a unicorn valuation less than a year after being founded.

But, beyond the market, Opontia has a very specific focus and strategy. And, it just so happens that I am friends with Co-CEO / Co-Founder, Philip Johnston.

Since it’s one of the most interesting stories in tech today, I recently caught up with him to dive into several topics around the Opontia story:

The Rise of the E-Commerce Aggregator

MENA’s Unique Opportunity

The Opontia Story

Why Opontia Can Win

So, strap in, as we glean product growth lessons from one of the fastest-growing, hottest e-commerce aggregators in the world.

The Rise of the E-Commerce Aggregator

Chapter 1 - Since the Earliest Days of the Internet

Since the earliest days of e-commerce, the concept of marketplace product listing sights has been hot. People have always wanted to bring the P&G or Unilever model online. But, P&G and Unilever themselves have been the last adopters of the internet. Their strategy is to minimize share loss of the online segment, but also not to cannibalize the more profitable in-person segment.

As a result, there has always been a marketplace opportunity for product listings. Things like Craigslist and eBay aggregated millions of small sellers and buyers. Then, it shifted to niche sites: Zillow with houses, Carvana for cars, and thredUP for used clothes. The biggest of these companies generally have a wide range of brands in one category.

Generally, Private Equity has stayed away from outright owning many of the small sellers who made a living on these platforms. The investments were viewed as high risk. Private Equity found dentists, law firms, hair salons, and the like to be less risky. They were less flash in the pan. They owned a physical store. They had assets. The small sellers, on the other hand, appeared like they could go bust as quickly as they went boom.

Chapter 2 - The Rise of Amazon and Shopify

The big shift was the rise of platforms like Amazon Marketplace and Shopify. They brought many of their small sellers along with them. Starting in about 2016, you started to see small sellers who were able to do $10M in a year.

Amazon, in particular, has been a gold rush. It might surprise you to know that fully 60% of Amazon’s business is actually these third-party marketplace players these days. I wouldn’t blame you. In 2009, that figure was only 30%.

60% of Amazon is a huge number. Marketplace Pulse expects 2021 will clock in at $300 billion of gross merchandise volume. That is big business, and there have been many winners. Shopify is an even bigger story, with 2021 GMV of ~$460 billion.

But, at the larger scale, the small sellers started to find themselves in tougher fights. For one, Amazon and the platforms are tough. The recent ‘Amazon Files’ found that the company regularly takes advantage of its marketplace providers, copying their products and giving its own preferable placement.

On another front, the retailers, especially big box, are not going to give up without a fight. Their market caps rely on a response, and they have followed up accordingly. Recently, Walmart reported 63% growth in its e-commerce business, and Target 144%. “Small sellers will want to have liquidity opportunities,” Maveron partner Jason Stoffer explains.

As a result of both the growth and the squeeze, the new hot game is to buy up those small sellers. It is a merging of the PE world with the world of small e-commerce merchants, and it has given rise to a new business model: the e-commerce aggregator.

From a strategy perspective, these companies see a perfect storm of: stable cash flows, attractive multiples, strong tailwinds, relatively easy growth levers, and relatively easy cost levers. As a result, many have sprung up quickly. As one founder explained, “there is a large pond, with a lot of fish in the pond, and an incredible number of sellers available for acquisition.”

Chapter 3 - Increased VC Investment in Aggregators

The opportunity to grow the revenue side and decrease the cost side has made the e-commerce aggregation business model irresistible for venture capitalists. Funding in the space has been on an unstoppable ascent.

2021 has been the cherry on top. These companies tallied over $2.5B in equity and $10B in debt funding for these types of companies.

Several large players exist. But one of the most remarkable things about them is that they were all founded since 2016. As a result, it is a game that is in its early innings. No winner has been crowned just yet.

Thrasio, founded in 2018, is the closest thing to a household name in the space. Depending on who you talk to, it might have been the fastest profitable company to reach Unicorn status early in its life. This year alone, it has raised over $1.6B. It has over 150 brands under its umbrella. In total, they offer over 22,000 products. The company has grown massively, fast.

What is the secret to Thrasio’s success? Former company executive Ari Horowitz explains that it is the “ability to take that marketplace data and do something smart with it. There was no ability to do that before. The genius was recognizing the data was there, as well as their ability to apply a layer of operations expertise to accelerate the business.” The company uses marketplace data and operational expertise to grow revenues and decrease costs.

As a result of these methods, the aggregators typically value potential targets on a multiple to seller’s discretionary earnings. This metric is in the spirit of adjusted expected EBITDA: it is the new bottom line the aggregator expects as a result of cost and revenue optimizations. Aggregators find targets in the 4-5x range, and then hope to fetch a higher multiple themselves as a result of synergies and diversification.

The key thing to realize here is that the aggregators usually are targeting profitable businesses, to begin with. This way, they can claim cash flow profitability while scaling rapidly. It is a business model that is growing more attractive to the investing class.

This alternative to a sales multiple, which many tech observers are used to in the SaaS world, reflects the greater uncertainty with aggregator investments. The business model is newer, and there is greater channel risk, especially with Amazon.

But aggregators, like Thrasio co-founder Carlos Cashman, argue that it is not in Amazon’s incentives to destroy its business. “Nobody looked at [Simon Property Group] as a competitor to Foot Locker — they’re not. They’re renting Foot Locker space for a store in the mall.”

In spite of this, many aggregators have been able to raise both equity and debt to fuel acquisitions.

But What Types of Companies Are They Buying?

The selection process is one of the most important for aggregators. In that way, it is not unlike the VC market. Because of its importance perhaps, the divergence of approaches is wide.

Some offer term sheets quickly and easily. All claim to. Some only go for cheap companies. Others are willing to pay high multiples. It all depends, and the market is as varied as it is new.

In general, the goal is to find companies with product-market fit but room to scale. Typically, the companies:

have a single person or very small teams,

have built their own brand,

and are not perishable.

As Philip pointed out, in one way, the companies aggregators are buying are easier to describe in terms of what they are not.

Most aggregators would steer clear of fashion, which is inherently trendy. Similarly, things that change frequently are less common targets. Staples like bathroom, toys, kids, and babies are large aggregator categories.

Similar to trendy items, aggregators also tend to avoid consumer electronics, where products are commoditized. A company like Anker went public on the back of marketplace electronics, and part of that is due to its scale economies from production, which nearly all one-person businesses do not have.

Finally, it is rare to see deals for companies that are not growing. This tends to be the anathema of the good trajectory selection criteria. Fixing a marketplace brand is possible, but more difficult than enhancing an already growing one.

To give a few more examples about the types of brands that have been making headlines, I have seen them in a few (not mutually exclusive) buckets. These are buckets where a one-man shop can actually win:

Niche Assortment

One of the areas these small brands have been able to succeed vis a vis the big box retailers and Amazon themselves is niches. They have the critical advantage of focus. They can get to know a specific target customer and build for them.

They might build for lovers of a very specific author, and create all the products for them. In that way, they kind of replicate the Fanatics strategy of licensed apparel but on a smaller scale.

Or, they might offer food options for a very specific segment, like Indian Americans. This is a group that has needs that might not be met by a big-box retailer’s items. Normally, they would go to a niche grocery store, like an Indian grocery store. The small target sellers replicate the Indian Grocery Store on the web.

Social Connection

Another area these small players tend to play is social. They may have a very specific social media presence that caters to users. Or they may have mastered a certain type of social media marketing, like TikTok.

The dancing cactus is an example of such a product. Although there are many mimic toys available, the cactus’ ubiquity in TikTok has helped its sales exceed others.

https://www.tiktok.com/@himums/video/7021180933785079042?_t=8OQc8JCN7Uc&_r=1

These types of companies leverage differentiated distribution to help their products take off on Shopify or Amazon. Many times, consideration of the importance of the founder to that channel weighs on the aggregator’s decisions.

Sustainable

The final common type of brand aggregators target is one with a sustainability value. Think Allbirds, but smaller. These types of brands offer a product from an environmental angle.

Eco-conscious consumers want to do good while shopping. These companies will often have a brand story, coupled with potential charity programs like Toms shoes. Many also use environmentally friendly products and offset carbon associated with manufacturing.

Of course, it is not just shoes. It is electronics, food, clothing, furniture, beauty, and everything else. Smaller products pop up everywhere and then become targets for aggregators.

The Unique Opportunity in Lesser-Known Markets

There are many large e-commerce markets. China at $850 billion, Europe as a whole at $800 billion, the US at $350 billion. But, what about the lesser-known markets? Opontia has its eye on CEEMEA: Central & Eastern Europe, Middle East, and Africa.

Central & Eastern Europe

Within Europe, there is a range of investment opportunities. Compared to their stage of development, Central & Eastern Europe have relatively low investment levels. It is hard to find aggregators or PE players buying up companies outside of Opontia. This makes the market cheaper on a relative basis.

Yet, there is quite a bit going on. Two really interesting countries are Poland and Turkey.

Let’s start with Poland. It has about $16B (US) in yearly e-commerce spending. The largest player on that market is Allegro. It is immensely popular, the #4 website in the country. Yet, 95% of its business is in the marketplace. Amazon is 60%. This makes it particularly target-rich for aggregation. There are thousands of sellers making a living on the platform.

Turkey’s e-commerce market is similarly sized to Poland, at $17B. You may have heard about it last fall when Trendyol, the top e-commerce site in the country, raised at a decacorn valuation. While Trendyol doesn’t share its portion of the business in the marketplace, it has a full-featured solution comparable to Amazon or Allegro, including last-mile delivery.

As Philip pointed out, many of today’s products are manufactured in one place and then shipped around. In much of Eastern Europe, many products are made in China. Turkey, though, is a producer nation. So, many of the marketplace targets in Turkey fully manufacture their products in Turkey.

Middle East & Africa

Outside Europe, opportunities for e-commerce aggregators are growing rapidly in the MENA region.

The Middle East has $30 billion of e-commerce GMV. Africa $25 billion. Though less mature than the west, both are amongst the fastest growing in the world. The number of sellers on marketplaces is growing by over 50% per year.

Saudi Arabia is a particularly interesting market. 55% of the population has an upper-middle-class or above standard of living. This population has a large appetite for e-commerce and is willing to pay a premium for premium services. It is driving an $8B, and rapidly growing, e-commerce market.

The e-commerce market is, as a result, rife with players from Haraj to Amazon. Like everywhere else in the world, marketplace companies play a large part for both Haraj and Amazon. For companies that can operate in the complex regulatory environment, the consumer is a strong one to serve.

The United Arab Emirates is also an interesting market. It has a small population, at only 10M versus Saudi Arabia’s 35M. However, the population on average is highly educated and well paid, with a GDP per capita of over $40K USD. As a result, UAE has a $5B e-commerce market, as well as a concentration of much of the overall MENA region’s top e-commerce talent.

Africa is also rapidly growing. South Africa is the dominant market (where domestic player Takalot is the e-commerce leader), followed by Nigeria, Ghana, and Kenya. Each is unique, with internet penetration and mobile banking penetration varying widely. However, one trait they all share is they are set to rapidly grow. Overall, the African e-commerce ecosystem is expected to double in the next 5 years to nearly $75 billion.

Many of you will have heard of Jumia, a public e-commerce player headquartered in Lagos, Nigeria. It is one of the players, but it is fairly niched with a $1000 average basket size. It is not quite like an Amazon in the US, Allegro in Poland, or trendyol in Turkey - with their sprawling selections and item coverage. Overall, Africa’s e-commerce ecosystems are not as developed as Central and Eastern Europe. But, in a matter of years, they are set to be.

Another thing these markets share is that Amazon is not particularly dominant. For Opontia, this makes them all the more attractive. It is playing where the highly funded players like Thrasio are not. This brings us to Opontia’s story:

The Opontia Story

Chapter 1 - Divergent Backgrounds

Philip Johnston was working in Venture Capital in Africa for Knife Capital and Blue Haven Initiative in the mid-2010s. He kept seeing e-commerce entrepreneurs who had started up interesting direct-to-commerce brands. Although he had to say no to most of the promising young entrepreneurs as a VC, he filed away the lesson.

There were many brands that would not be attractive for a VC return profile, like a kitchenware brand. The entrepreneurs have reached a point where they cannot grow without the support. So there was a gap in the market. Philip realized that the model which was growing in popularity across the US and Europe, was needed in lesser developed regions.

Manfred Meyer, meanwhile, had spent 10 years working as an executive and consultant in the e-commerce space. After managing Lazada’s Malaysian presence, he spent two years as Chief Commercial Office for Digikala, the largest e-commerce player in Iran. The business actually grew to be the largest by revenue in the Middle East, until the West began to restart sanctions and Manfred moved on to the next step.

He moved to Dubai where he set up an e-commerce enabler. Entrepreneurs paid Manfred’s team a fee to help with listing, commercial management, warehousing and fulfillment. There, he developed deep insight on the market and struggles of solopreneur marketplace companies in the region.

Chapter 2 - Connection to Funding in 14 Days

Between the Digikala and consulting experiences, Manfred also saw the potential for a new acquisitive, strategic e-commerce company, focused on entrepreneurs in the region. So, at the beginning of 2021, when Philip reached out through a mutual VC friend connection, Manfred was all ears.

By that time, Philip had completed his two Ivy League graduate degrees and spent 2 years at McKinsey in Dubai. He had been vetting startup ideas with his VC friends since the end of 2020. Many of the ideas received a lukewarm reception.

But when Philip proposed an e-commerce aggregator in markets without them, VCs were ready to make verbal commitments then and there. The reception was a world’s apart, and Philip was on a mission to build the company.

The meeting with Philip and Manfred would, as you know, of course, end up being fateful. They both brought a shared context of immediately “getting it.” So many times, with a wild idea no one has done before, the concern is whether it will work. These two understood, with the right execution, the opportunity was there.

Rather in the spirit of 2021, Manfred had come down with Covid at exactly the time Philip reached out. But the first meeting itself, the two clicked. They would go on to have a series of 4-hour Zoom meetings and knew they were ready to do business together.

A particularly good signal for the two was their contrasting experiences and expertise. With his VC, MBA, and consulting background, Philip had a financial background. He spoke the language of multiple expansion and how to purchase the businesses at attractive multiples and grow them together to create greater enterprise value.

With his deep experience on the ground with Middle Eastern e-commerce, Manfred covered the operations of selling online. He spoke the language of Stock-Keeping Units (SKUs) and what it takes on the ground.

It was a match ready to drive enterprise value. With the core team in place, the duo went out to turn the verbal commitments into paper ones. In one of the fastest seed financing ever, a week later the company had secured several million dollars to get going. As Philip said:

The whole process was the quickest fundraise you can imagine. It was insanely fast.

Perhaps the key lesson for other entrepreneurs from Opontia’s founding moment is that you don’t have to pursue the idea you’ve been passionate about since you were 7. Philip and Manfred found an idea that VCs wanted to fund and others weren’t doing. They found “company-funding” (versus product-market) fit.

After raising the round, the two finally met in person:

Originally conceived as a business that mainly focused on the Middle East and North Africa, it was off to the races for the young startup.

Chapter 3 - The Polish Opportunity

As the duo began evaluating deals, one of the first realities the team encountered was the difference between strategy and execution. Many great deals that were coming their way, looked to be based in Poland.

As I mentioned a few thousand words ago, Poland’s leading e-commerce marketplace, Allegro, is not only large but 95% of it is marketplace companies: small sellers that are targets for aggregators like Opontia. And, despite the large numbers of sellers that were driving that huge business, there were very few acquiring companies looking at them.

As most strong young companies tend to do, the company pivoted its focus. It has begun acquiring companies in Poland. Instead of viewing CEEMEA as disparate markets, the larger strategic driver picture for the company is targeting marketings where there are no other players acquiring. This allows Opontia to get more attractive prices and build an operational moat.

One of the drivers of the lack of competition is that Amazon does not have a presence. The story with Thrasio and others is typically centered around Amazon. In Poland, Amazon has around 2% market share. In Turkey, Amazon has less than 10% market share. This makes it less likely Amazon-centric players will join soon.

It also helps that they are in the same timezone.

Chapter 4 - Executing

Since identifying its larger strategy of acquiring in less competitive markets, the company has scaled to open up more offices beyond Dubai in Poland, Turkey, and Saudi Arabia. The worry with that level of scaling is if the team is going too fast. Less than a year old with four offices could be a recipe for unsustainable costs.

From Opontia’s vantage point, this is the general story in the industry. The aggregators are buying up profitable businesses. They do not need to translate a product and translate a new regulatory environment to operate in a new country.

Instead, they hire a lean team - a general manager and business people to track down the opportunities - then they get to purchasing. As those brands are established and the entrepreneurs behind the companies leave, the company builds out the marketing, brand, and other functions to grow the businesses in a just-in-time model.

To lead operations across all the brands, Opontia hired a former executive from Jumia. As VP of operations, he keeps the companies running after the entrepreneurs leave.

Opontia is focused on being seller-friendly. As it is for most aggregators, it’s an acquisition strategy.

One of the most important vectors for competition in the aggregator space is seller friendliness. As a result, the team also spends a good deal of time being upfront with sellers and then following up with those promises. Selling your business is not for everyone.

Like many aggregators, Opontia does offer companies participation in the upside. Most sellers expect to make about as much in these earn-outs, calculated based on profit, as the initial selling price.

One of the early success stories for the Opontia team has been Novimed. Opontia has managed to quadruple Novimed’s sales and doubled profits in just 5 months since its acquisition. The UAE-based direct-to-consumer company operates in the health space. Its success has created momentum for Opontia to purchase more companies.

Chapter 5 - Series A and More

Last month, the team announced that it had raised $42M to further fund its aggregation strategy. Impressively, Saudi Telecom’s venture arm, the largest VC fund in MENA, led the equity portion of the round. In addition, existing investors Raed Ventures and Global Founders Capital doubled down. A little over half the round was venture debt from Partners for Growth, an SF venture debt fund.

As Saed Nashef, a participant in the first round and now board member said:

We’ve made an early bet on Opontia in their first institutional round purely on the strength and experience of the founding team, and the size of the opportunity in the consumer goods aggregator category. Philip, Manfred, and their team have done an amazing job at establishing Opontia as the leading sellers' roll-up player in Mena.

The company is hoping to live up to the praise of being the leading sellers’ roll-up player. As of writing, the company has over 50 employees and signed deals with over 15 brands.

In the coming months, Opontia expects to open offices in Egypt, Nigeria, and Pakistan. After that, it may even look at the Nordics and Russia. The team is thinking big, and big rounds are in their future, or so they think:

Why Opontia Can Win

The Strategy

Part of the appeal of the aggregator strategy is to streamline back-end logistics and simplify distribution across multiple product categories. While it’s possible for individual businesses to master this complex web of systems, aggregators can have a real advantage by going deep in those areas.

Opontia is focused on back-end logistics and distribution, but it also considers a wider array of potential growth levers:

Added working capital

Expand geographically

Expand product line

Expand channels

Enhance digital marketing

Grow the brand

Based on what’s working, they double down on that. So, this enables multiple growth trajectories to grow the business. If a company has a really resonant message in digital marketing channels, Opontia will pour in the cash. If the product can work elsewhere, Opontia takes it there.

The work and strategies are adding up. Philip and Manfred’s expertise help. Philip can provide the McKinsey and financing perspective and Manfred the e-commerce perspective. They have also built out a strong team of e-commerce veterans around them. The company just crossed 50 employees. In four to five months, the company expects to have acquired about $30M in run-rate revenue.

The Portfolio

Opontia has acquired four brands and signed term sheets with 15 more. With the added capital and growth plans, the dream is to multiply those numbers.

While we can’t predict the deals it will find then, analyzing the company’s current products, it has a focus on “all-weather” products that do not face seasonality. Things like kitchenware, bathroom, cosmetics, and toys.

Specifically, the companies Opontia has been public about include:

Orthopedic pillows

A perfume brand

Traditional dress for Kids

Baby swings

Bath bombs

It is an eclectic mix. This goes to emphasize that Opontia’s model is quite different from the average roll-up or product listing site. It is acquiring different businesses that market to different audiences. Then, it is scaling each of them as brands.

Opontia also shared that they were indeed all companies that were growing, not perishable, and built by a single entrepreneur. It has stayed close to “high quality” selection criteria instead of “fixer-uppers.”

What Will the Future Hold?

With competition rebranding themselves as supporting founders, or others offering Teslas for referrals, the e-commerce aggregator space is red hot. Keith Rabois has even entered the space with his company OpenStore, focused on companies using Shopify’s tools.

This makes some worried that valuations are getting overheated. The thought is some startups are in for a tough future once the money dries up.

The Opontia team is not listening to the noise. They are just focused on executing. The founders I met with tend to agree more with the sentiment of General Catalyst partner Mark Crane, “This is one of the largest markets we can think of outside of infrastructure, software, and health care.” Because this is such a large market, there are bound to be many players.

They also are students of business history. They have heard the warnings for years from business academics that roll-up strategies tend not to work. As the Harvard Business Review judged, two-thirds of roll-up strategies fail. The pseudo-adjacencies, synergy mirage, and financial engineering just clog up otherwise profitable businesses.

Manfred and Philip are mired into the details to be part of the one-third.