How to Build a Neobank: the Nubank Story

The world's largest neobank IPOs today

Hey friends! Since Nubank IPOs today, you are getting a midweek dispatch of the newsletter - my piece on Nubank. I am also including a special piece on, “So, you want to DAO your company?” below. I hope you like the pieces.

Reminder to share with your friends! We increased subscribers by 10% over the last few days 🙏

How to Build a Neobank: the Nubank Story

Nubank is one of the buzziest FinTechs around. Over the last three years, it grew from 3.7 million customers to 48.1 million customers. That’s a 100% CAGR in new customer additions. It looks like your typical exponential hockey stick:

For size perspective, Bank of America only has 40.0 million digital active users of its consumer banking services. Nubank has more digital customers than BofA. It is now the largest neobank in the world.

But how did NuBank become the world's largest neobank? What lessons can builders, fintech analysts, and product leaders take from its story? As the company is about to IPO, let us learn more about how to build a neobank.

Phase 1 - Origins

This story starts, like so many tech giants, with a Stanford graduate.

After growing up in drug-torn Medellin, Colombia, David Velez’s family escaped to Costa Rica when David was 9. There, he studied in German-language prep school and graduated as valedictorian, earning him a trip to Stanford for his undergraduate studies. After completing an engineering degree and a few years in banking and private equity, he returned to Stanford for his MBA.

Upon graduating, he headed to Brazil to build out the Venture Capital firm Sequoia’s to Latin American business. It was the perfect next step for the budding technologist. Or so David thought. Mere months after relocating to Latin America’s largest economy, Brazil, Sequoia pulled the plug on the Latin American experiment.

It turned out to be a good learning experience for the entrepreneur nonetheless. David got to intimately learn the structure of industry in Brazil. And he had one great realization:

What’s the biggest industry in Brazil? Banking. And what’s the most profitable banking?

After years of inflation, interest rates were high. Being a bank was a highly profitable enterprise. Not only was banking the biggest and most lucrative industry in Brazil, it was also highly concentrated. 5 banks controlled 82% of the market. As a result, the customer experience was horrible.

David experienced this subpar user experience first-hand. When he moved to the country, it took weeks of waiting in-person, and filling out myriad forms, to do basic financial activities. It was a far cry from the US, or even his native Colombia, or childhood home Costa Rica. It was actually terrifying:

I remember getting locked in those bulletproof doors a couple of times because I had my cell phone in my pocket and guards looking at me with guns

This is the first lesson from NuBank’s story:

Lesson 1: Find a Market Where Large Players Deliver Bad Experience

Of course, if you find such a market, there will be reasons. The existing locals will have been too shy to build a business. They can see all the structural barriers that the market dominating incumbents have put up, and it scares them. David was undeterred. As he says:

Nubank could never have been started by a local… It required a Silicon Valley investor who has seen this story of the tiny ant going against the elephant and succeeding. A Latin American investor sees that and says, ‘No way, the elephant is going to crush you.’

The digital transformation that was sweeping Brazil in the early 2010s was clear for anyone to see. But only David seized the opportunity to create a company.

He began the process of working on a neobank in Brazil. He connected with industry insiders. He networked with other upstarts like Capital One in the US and ING in Europe. He learned the trade secrets. Armed with this information, he formed the initial Nubank strategy: they would offer credit cards that beat the big banks on fees and convenience.

After raising a $2M seed round, Sequoia partner Roelof Botha convinced David to find co-founders. In searching, David met Cristina Junqueira. An engineer with an MBA from Northwestern who had been heading up one of the big 5 Brazilian bank’s credit card division. She was the perfect fit to navigate the Brazilian market.

To enhance the tech bonafides of the business, David turned to a contact from his Sequoia days. He had met Edward Wible, a Princeton Computer Science grad with an MBA from INSEAD. The three co-founders would make the ideal trifecta to conquer the Brazilian banking landscape.

The trio rented a house in Sao Paulo and got to work. In August, 2014, they raised a $15M series A. They launched Nubank’s beta a month later, with the primary value proposition being credit card with no annual fees. It did not need a banking license to launch a credit card. To this day, that is its largest revenue driver, the interchange and interest fees from its credit card business. It was a case of prescient instincts from the start. The existing products were horrific. Brazilian credit cards had interests running 200% to 400% a year.

On top of that, they charged annual fees. The lowest competition was $20. Nubank was free. That is the second lesson from the Nubank story:

Lesson 2: Start With a Product With Comparatively Bad Terms

In addition to having better terms, Nubank provided a better user experience. In contrast to the crazy lines and terrifying guards David had experienced banking at a traditional player, Nubank was fully through the app. Suddenly, using a credit card was simple.

To get the rest of the story, smash that red button:

So, you want to DAO your company?

They Said, “Let’s Buy the Constitution”

It was the auction featured on newscasts around the world. A copy - yes a copy, not the original document - of the US constitution was going up for sale. As far as utility to the world, the value of the document was as a historical artifact and collector’s item. Yet, it was featured everywhere from Forbes and CNBC to NPR and the New York Times.

What was so newsworthy about another Saturday afternoon auction at Sotheby’s? A group of 17,437 contributors from across the world had pooled together their money into a Decentralized Autonomous Organization (DAO) to bid on the historical document.

There was only one problem. The group gave away their reservation price for the world to see. They had put together $43 million for the document. An anonymous private collector, who was later revealed to be the evil villain of the year’s Robinhood scandal Ken Griffin, just barely outbid the group to secure the artifact.

And if you thought the story ended there, you would be wrong. That is just where the mainstream news stopped reporting.

The constitution DAO did not just end. Participants were given two options after losing the auction: redeem your $PEOPLE tokens and lose money to gas fees, or claim the token and keep it in your wallet. Many opted to keep the token. And its price has surged:

As of writing, the token has a market cap of $610M. If you had put $2,500 dollars into the constitution DAO - the average amount - and held your $PEOPLE tokens, they would now be worth about $30,000.

Did you earn $27,500 last month?

There is clearly more to the story of the constitution DAO, and DAOs in general. Indeed, every product and strategy leader worth their salt is asking themselves: should we do something with DAOs at our company? This article is here to help you with that.

To get there, we’ll explore:

History of DAOs

Major DAOs Today

The Future of $PEOPLE

Applications of DAOs to Companies

History of DAOs

To better understand how you can use a DAO at your company, it makes sense to have an understanding of their history.

Like most things in crypto, DAOs have their origin from Vitalik Buterin, the founder of Etheruem. Vitalik began writing about them in his prolific crypto writing phase of 2010-2012. Then, in 2013, Vitalik included a definition of DAOs in the Ethereum Whitepaper:

A virtual entity that has a certain set of members or shareholders which, perhaps with a 67% majority, have the right to spend the entity's funds and modify its code.

In typically Vitalik fashion, the definition is deceptively simple. Its straightforwardness betrays its prescience. Beginning with “a virtual entity,” Vitalik gives a good primary subject to the term: a group of people organized on the internet.

Then, when he describes the mechanic of consensus to change code based on majority ownership, it gives the blueprint for everything DAOs have become today. DAOs enable voting through collective ownership. Majority gets the right to change the code. With the power of Ethereum’s smart contracts, this means the majority get the right to make the decisions.

There is no legal entity, or employment contracts. Instead, there is machine consensus around token governance rulesets.

In 2015, early groups began getting together. One such group was MakerDAO, whose $DAI token has a market cap of $6.5 billion as of writing.

But it was not until 2016 that the world really saw the first DAO out in the world, called The DAO, and also referred to as Genesis DAO. It was meant to operate as a decentralized venture capital fund for crypto. It had a creation period, which allowed people to exchange Ether sent to a wallet address for DAO tokens. The creation period went unexpectedly well. It gathered 12.7M $ETH, worth $150M.

Unfortunately, a few days after the creation period ended, hackers found a crack. The group walked away with $70 million unrecovered. This began the spiral towards Genesis DAO's ultimate demise. The DAO’s public failure was a setback for the space. Compared to ICOs, DAOs made relatively little noise in the crypto boom of 2017.

But, ultimately, DAOs roared back from the “DAO winter,” in 2019. In January, 2019, MolochDAO released to fund infrastructure projects on Ethereum. This kicked off what is known as, “the year of the DAO.” Several now prominent DAOs were born.

Major DAOs Today

The momentum has continued strong. And these days, there are hundreds of DAOs managing tens of billions of dollars in assets. The past three months have been particularly monumental, with assets locked (popular crypto metric TVL) into the ecosystem doubling from ~$7B to $15B.

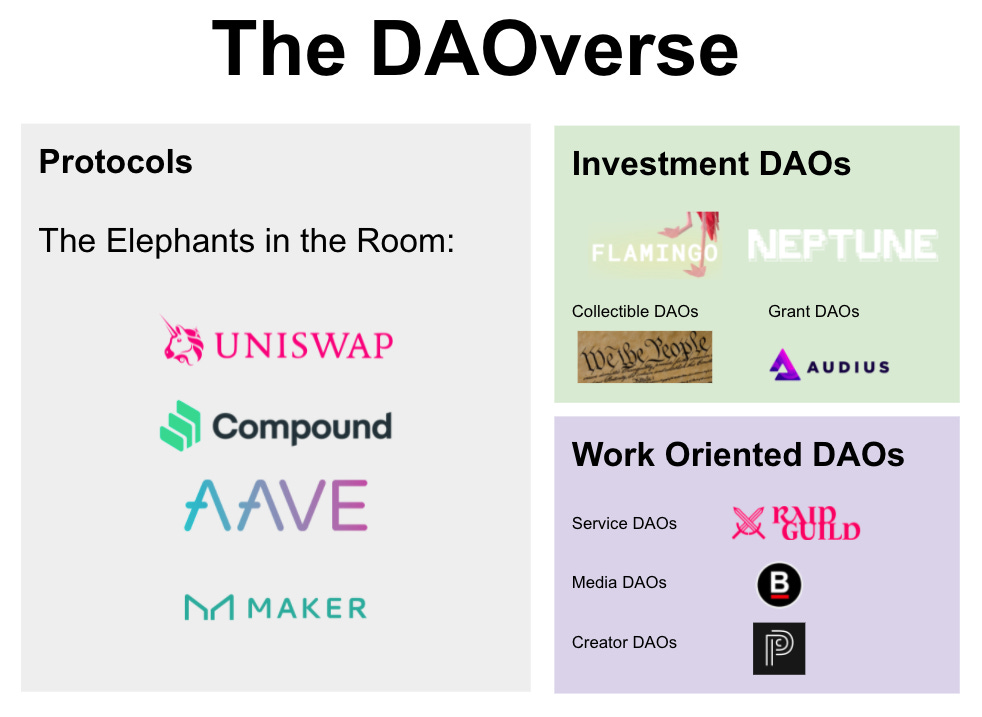

It is worth understanding the main types of DAOs behind this explosion in value.

The most prominent group is protocol DAOs, encompassing all of the top DAOs by market cap. These look and feel quite different from the Consitution DAO. This group includes Uniswap, which I wrote about a few weeks ago, the largest decentralized exchange (DEX). If you recall, Uniswap is a protocol: a way to create liquidity for long-tail trading pairs. Its governance token $UNI currently has a market cap of $11.6B. That’s more than the highly talked about failed Zoom acquisition Five9, which has a market cap of $9.7B.

This protocol group also includes AAVE, whose $AAVE governance token has a market cap of $2.7B. That is more than recently IPO’d Allbirds, which has a market cap of $2.2B. Aave’s protocol for borrowing and lending plays a similar role to money markets in traditional finance. It enables token holders to deposit them into liquidity pools while earning interest in real-time. Other users can borrow the assets through Flash Loans, which require no collateral.

Another prominent protocol making waves in the world of decentralized finance (DeFi) is Compound. Compound is an interest rate protocol. It creates a floating, short-term interest rate for assets. This allows anyone to borrow assets. Further, interfaces built atop Compound’s protocol, like Compound Treasury allow users to simply earn 4% APR on USD without any crypto complexity. The DAO’s governance token, $COMP, has a $1.4B market cap. That’s nearly double the market cap of recently IPO’d Rent the Runway, which currently has a $700M market cap.

Where do DAOs come into these protocols? They are the consensus mechanism to govern the code changes. Nowadays, their code is heavily publicized and audited at cost. This helps to prevent hacking and trust problems, like encountered with the Genesis DAO.

Then, there are a bunch of DAOs that are more similar to what we think of with Constitution DAO and Moloch DAO, made for investing. These are investment DAOs. They pool together cash to make purchases they could not have individually. Prominent examples include Flamingo and Neptune, which each are worth over $25M with the $ETH added. There are also subcategories of collectible DAOs, focused often on NFTs, and grant DAOs, often focused on a web3 objective. Some in this group are primarily social; others, primarily returns-focused.

Then there are a bunch of more work oriented DAOs. These include service DAOs. These operate dev and design agencies for web3. The canonical example is RaidGuild. It also includes media and creator DAOs. These create content. Prominent one’s include Bankless, cited in this piece, and Personal Corner.

This overview of the landscape of the DAOs can help us better contextualize how to build for companies. But, just before we get there, let’s return to Constitution DAO.